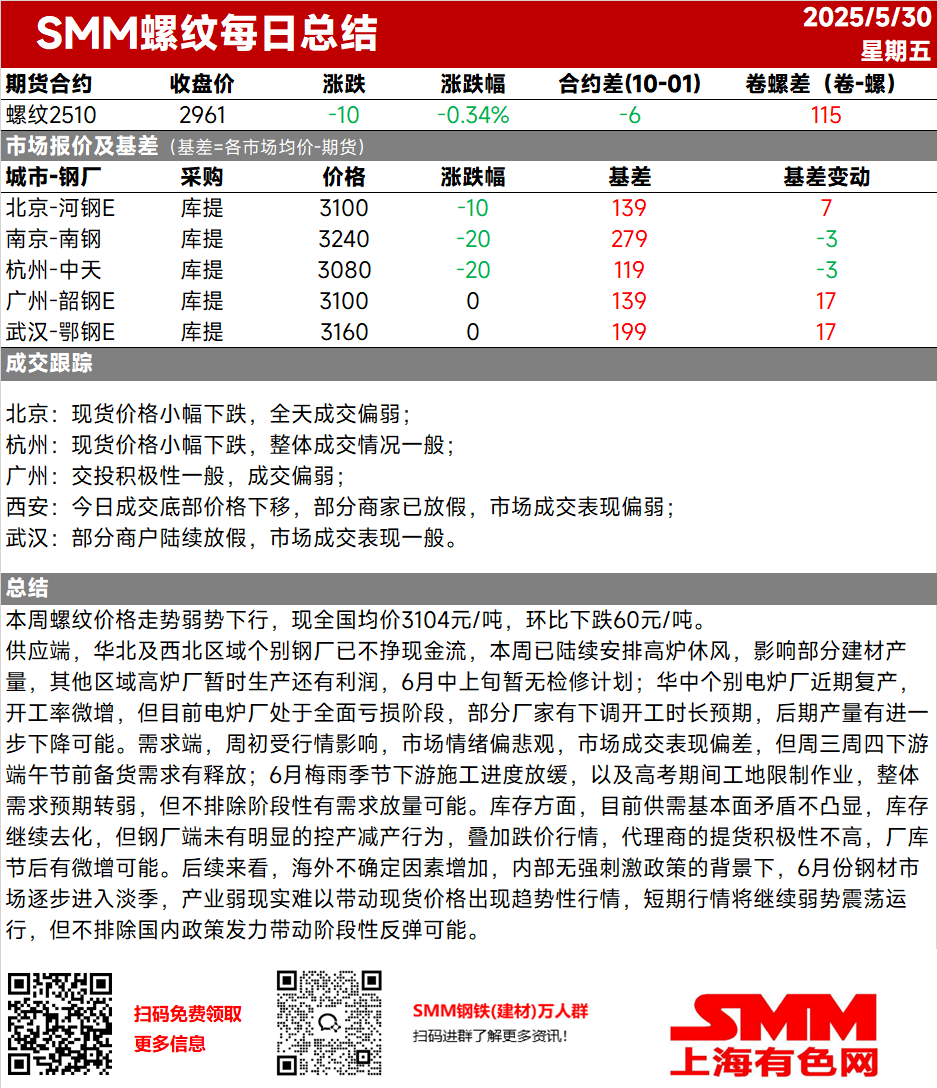

This week, rebar prices showed a weak downward trend, with the current nationwide average price at 3,104 yuan/mt, down 60 yuan/mt WoW. On the supply side, individual steel mills in North and North-west China are no longer generating positive cash flow and have arranged for blast furnace maintenance this week, affecting some construction steel production. Blast furnace mills in other regions are still profitable in production for the time being, with no maintenance plans scheduled for the first half of June. Some EAF steel mills in Central China have recently resumed production, leading to a slight increase in operating rates. However, EAF steel mills are currently in a phase of overall losses, with some manufacturers expecting to reduce operating hours, suggesting a potential further decline in production in the future. On the demand side, influenced by market conditions at the beginning of the week, market sentiment was pessimistic, and market transactions were poor. However, downstream stockpiling demand before the Dragon Boat Festival was released on Wednesday and Thursday. In June, during the plum rain season, downstream construction progress will slow down, and work restrictions will be imposed on construction sites during the college entrance examination period. Overall demand expectations have weakened, but there is still a possibility of periodic demand surges. In terms of inventory, the current contradiction between supply and demand fundamentals is not prominent, and inventory continues to deplete. However, steel mills have not taken significant actions to control or reduce production. Coupled with the falling price trend, agents' enthusiasm for picking up goods is low, and there is a slight possibility of an increase in in-plant inventory after the holiday. Looking ahead, with increasing uncertainties overseas and in the absence of strong stimulus policies domestically, the steel market will gradually enter the off-season in June. The weak reality of the industry makes it difficult to drive a trend in spot prices. Short-term market conditions will continue to operate in the doldrums, but there is still a possibility of periodic rebounds driven by domestic policy efforts.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)